Credit cards are a tool, and like any tool, they can be very useful when used properly, or cause bigger problems if used incorrectly. They are not to be feared if you understand how everything works, and follow a few basic rules.

What are credit cards?

When you sign up to a credit card, an institution gives you access to a line of credit which is typically intended to be used to fund your purchases for a short term. You spend within your agreed credit limit, then pay the balance off in full by the payment due date. You are borrowing money to fund your purchases now, and repaying the credit card provider at a later date.

A common misconception is that the only way credit cards make money is by charging you interest and late payment fees. And whilst that is the biggest revenue stream, card issuers also receive a share of the merchant fees paid whenever you use your card, and some other usage fees. Following some basic rules you get all of the benefits of a credit card, without any additional costs. The credit card company still makes money and you’re not being a “bad customer” for paying off your balance in full.

There are also other fees like currency conversion fees if you use the card abroad which you need to know and navigate correctly to avoid paying them.

Risks

As much as we’ll make a case for why credit cards are useful in this article, they are not for everyone.

Credit cards have been shown to increase spending, as paying feels less immediate. Fees and interest will become an additional expense if the card balance isn’t repaid in full.

You know yourself better than we do, so if you think that there’s a risk of increasing your spending, or getting into situation where you have to pay interest and fees, you should avoid getting a credit card.

Making purchases you wouldn’t otherwise make, and paying interest could throw off your budget and cancel out any benefits you receive from using a credit card.

✓ GOLDEN RULE

Don’t let a credit card change your spending habits –

Never spend money you don’t have.

Always pay off the full statement balance.

Why use them?

Credit cards have a number of advantages over debit cards and cash, so provided you get the right card and know exactly how to use it, it can be a great primary payment method for a number of reasons.

Fraud protection

Arguably the most important benefit is the fact that credit cards offer you better protection on your purchases when compared to debit cards (and certainly cash). You might think that they are both “cards” or “Visa/Mastercard” but there are actually separate laws specifically for credit cards which give you extra protection.

Section 75 of the Consumer Credit Act 1974 is what gives you this extra protection. Read up on it to know when it’s most beneficial to use your credit card and what rights it gives you, but the idea is that it ensures that you receive your good or services, they are as described and are not faulty. American Express takes this a step further and even covers accidental damage or theft of items under £2,500 for 90 days, amongst other benefits.

This usually applies for transaction between £100 and £30,000, and even if only a part of the purchase was paid for with your credit card.

Section 75 does not apply to debit card transactions, though there is a potential workaround for this (using Curve).

Travel

Some credit cards don’t charge foreign transaction fees, making them ideal for spending abroad. If you regularly travel, see our travel card guide.

A lot of neobanks now offer free cash withdrawals and near interbank exchange rates too, so these may be your best option, particularly as cash withdrawals from a credit card aren’t ideal.

Cashback

Cashback may be one of the best known perks with credit cards, and particularly American Express.

Cashback is a great perk and definitely something that we highly recommend you look for when getting yourself a new credit card. Essentially, everything you were already planning to buy is reduced by 1% with just a small change of habit. You are indirectly recouping some of the transaction fees that the merchants add to the sale price.

You should do most of your spending on a cashback card, but consider all the benefits and make sure you know all the fees associated with your cards, otherwise you could cancel out any cashback received. An American Express card might pay you 1% cashback and be your primary card, but it will cost you 3% to use abroad for example.

Some cards offer points, some offer variable cashback rates depending on where you spend, and the rates differ from card to card. Have a look below for our opinions on the best cashback cards and the benefits they offer.

Short-term cash flow

As purchases are typically interest free for 25-56 days, credit cards are great for cashflow, essentially giving you a buffer between your purchase and the money leaving your bank account.

Whilst your money stays in your bank, you spend on your credit card during the month, then pay the balance in a single transaction when it’s convenient.

Time value of money

If you’ve read our article on inflation you’ll understand this concept quite well. As money devalues, prices go up, but the cost of your debt goes down.

As long as you avoid paying interest on your credit card, your money can remain in your bank account or investment account longer, earning interest.

Deposit for car rental/hotel

When you rent a car, and don’t take out full cover from the rental company, they’ll typically require a deposit somewhere in the region of £1,000. This isn’t taken off your card but it “authorised” which just means that they check that you have enough credit for it and reserve it until the end of the rental just in case they need to take it at the end.

This can usually only be done with a credit card. If you don’t have a credit card with a high enough limit, the rental company will force you to purchase full insurance from them, even if you have your own, which may more than double the cost of your rental.

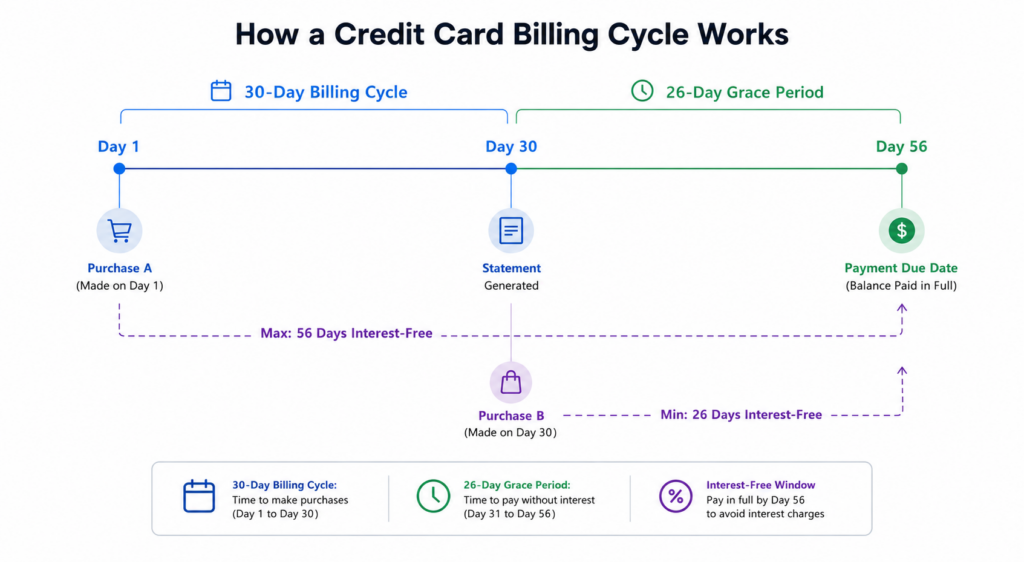

How repayments work

Your statement period is typically a month, starting from the date your application was approved. At the end of your statement period, a statement is generated with the total you owe for the month. This will show your statement balance – the total amount that you owe for the period.

The statement balance is what you need to pay off in full, and it is not to be confused with your “current balance” which you might see on the credit card website or app. That amount includes pending transaction and transactions in the new billing period. You do not necessarily need to have your entire current balance paid off, as that will be paid off in the next statement period.

You are given a grace period of about 21-25 days to make the payment, and at the end of this is your payment due date. This is where the ~56 days interest free period comes from – if you make a purchase at the beginning of your statement period, and pay it off on your payment due date, that payment should not incur interest for the statement period plus the grace period, i.e. a maximum of 56 days.

The statement should show two amounts, a minimum amount payable, and your statement balance. The minimum is usually £5 or 1-3% of your statement balance, whichever is larger. You have to pay the minimum amount to avoid the missed payment fee, and you have to pay the full statement balance to avoid getting charged interest. If you do not pay the full amount by the payment due date, you will start paying the APR on the outstanding balance – this adds up quickly and is why you must pay off you balance in full every month.

Example:

- 1st Jan: £50 purchase

- 30th Jan: £50 purchase

- 31st Jan: statement generated with £100 balance. £5 minimum payment

- 25th Feb: payment due – paying the full £100 balance before then means no interest

Direct debit – when you are first setting up your credit card, it will have some options for paying off your balance. The credit card company will ask to setup a direct debit from your bank account, and will give you the option to take the minimum payment or the full statement balance. Simply select full statement balance and this will avoid pretty much all unnecessary fees.

When the payment is due, the full amount will be paid off via direct debit and you won’t owe any interest or late fees.

Paying only the minimum means the remaining balance continues to accrue interest, and it can take years to repay larger balances as the interest compounds.

Credit score

If you have a low credit score, it could mean your credit card application getting rejected, or receiving unfavourable terms, as is the case with other credit products and services. You may be offered a lower limit and a higher APR to begin with, and this may increase as your score improves or you build trust with the company directly.

You can check your score yourself before any credit card application to gauge the odds of you getting accepted for a particular card. You should always have an option, though may need to start with a “credit builder” credit card in some circumstances.

Lenders will use their own criteria along with any information they receive from the credit agencies, so your exact “score” is not something you should spend too much time thinking about. It is an indicator they use, rather than it being a simple pass/fail score.

How you use your card once you have it will also impact your credit score. Utilising too much of your available credit, missing payments, or cash withdrawals can all have an impact on future credit applications.

Your credit score is quite big topic in itself, so you may want to read our dedicated article on that to get a better understanding.

Credit limit

The credit limit – the maximum amount the credit card provider will lend you – is not really something you choose yourself. The limit you receive will depend on many factors such as your age, your credit score, your credit history, existing debt, etc. If it’s your first card, or you’re young, or your credit score isn’t great, a card provider will likely offer you a lower credit limit (and a higher APR) when opening your account. They may then increase this limit automatically, or if you request a higher amount, after some time.

Fees

APR

APR or Annual Percentage Rate is the headline figure you see most often with a credit card. This is essentially the interest rate at which the company will lend you money (provided you don’t pay off your balance in full every month). So let’s say the APR is 30%, and you keep a balance of -£100 on you card for an entire year (NOT recommended), it means that after a year you will have accumulated somewhere around £30 of extra debt and your balance after a year will be more than -£130 as the APR does not consider any other fees you might have been charged if you didn’t make the minimum payments over the year.

The rate you receive will depend on the credit card company, your credit score and various other factors such as how much credit you want, your financial situation, etc. Of course you always want to go for the lowest rate available, but if you repay your balance in full every month, the card benefits offered should be more important than the APR.

A credit card typically gives you 25-56 days after a purchase before you are charged interest on that purchase (statement period plus grace period as described above). This means that if you pay off your monthly statement balance IN FULL, you don’t pay any interest and essentially receive free credit.

If you have credit card debt that you cannot pay off, consider a balance transfer card offer which will give you 0% interest on debts you transfer to the new card for a certain period.

A typical APR will be 20-40% depending on the card and your situation. The representative APR you see advertised is the rate offered to over 50% of customers.

Monthly/annual

Most credit cards don’t tend to have monthly fees, so if you don’t use your card and don’t have an outstanding balance, you’ll have nothing to pay. Other cards will charge a monthly fee, and in return usually try to offer you some additional benefits (which you may or may not use).

Cash advance

Credit cards are intended to be used for payments of goods and services, not for you to use as a cash loan. Therefore, if you withdraw cash from an ATM, most cards will charge quite a hefty fee for the withdrawal.

Additionally, unlike standard transactions, interest starts to accrue straight away on cash withdrawals. Certain other transactions such as cryptocurrency purchases, lotteries, investments and wire transfers are also considered “cash-like” and will be treated in the same way.

A cash advance may also have an impact on your credit score as it’s may be seen as a desperate measure to acquire cash.

Therefore, it’s generally best to avoid cash withdrawals from your credit card.

Foreign transaction fees

If you use your card abroad, or even just purchase something online in a different currency, a lot of cards will add a currency conversion fee (typically around 3%, and potentially a minimum fee of £1-3 per transaction), and maybe an additional flat fee per transaction.

There are a number of cards which won’t charge usage fees abroad, and exchange the currency at near perfect interbank exchange rates. This makes them ideal for using abroad for all of your purchases as it will work out much cheaper than exchanging paper currency before you go away.

If you’re using your card abroad, remember to ALWAYS select the local currency (no conversion) if given the option, to get the best rate. The rate which the merchant offers you will often add a premium of anywhere up to 20%. I.e. for a €100 purchase, they might offer to charge your card £95 (with conversion) or €100 (without conversion) – your bank should exchange that €100 themselves at a better rate and charge your account about £86.

A lot of neobanks offer similar benefits in terms of being free to use abroad and offering other perks, so are also a great option when you are abroad.

Balance transfers

A balance transfer allows you to transfer your existing debt from one card to another, to potentially take advantage of a promotional 0% interest rate.

Though this could give you the necessary breathing room to clear your debt, it should be treated as a temporary emergency strategy rather than a long-term solution, as a credit card balance should never be carried long term.

The fee is typically 2-5% of the transferred amount.

Penalties

In the UK, most penalty charges are usually £12, as credit cards must not charge “excessive” fees.

Missed payment fee – if you fail to make the minimum payment for the month.

Late payment fee – as with missing your payment entirely, you are charged a fee and interest is charged on the outstanding balance.

Returned payment fee – similar to the above, but if your bank rejects your monthly payment to pay off your credit card due to insufficient balance or another reason.

Exceeding your card limit – though your card transactions should decline if it would put you over the limit, other card charges and penalties could push you over.

Next steps

- Having read the article, you should decide exactly what you want to get from a credit card, if you know that you can repay it in full every month and not have it cause an increase in unnecessary spending. Then decide on the card or combination of cards you think would best suit your needs.

- If you’re not sure what your credit score is, you could sign up to a credit score provider which would give you an idea of what you may be able to get, or if you might need a credit building card first. Credit score providers will try to offer you plenty of credit cards but from our experience they’re not the best cards around as they have high APRs – have a look through the article above for our top recommendations.

- Once you’ve made your decision on which card or cards you want, just go ahead and sign up. If you’re thinking of signing up to multiple cards, read through our Credit Score article to see if you might want to spread your signups over a few months to avoid your maximum credit jumping up too quickly if you think you might be getting another credit product anytime soon.

- First thing you need to do once you’ve received your card is to setup a direct debit to repay your statement IN FULL every month. This is the best way to minimise fees. Read all of the conditions of your card to ensure that you understand all of the fees, perks and conditions.

Conclusion

Get a credit card, spend on the credit card to take advantage of any perks and benefits, pay it off IN FULL every month. Don’t let it increase your spending, so if you know yourself and think that that might be a possibility, it is not an absolute necessity and you can find yourself alternative debit cards for your needs.